Stockbroker vs. Investment Adviser: Understanding the Difference

What is the difference between a stockbroker and an investment adviser? The Securities and Exchange Commission has found that many investors do not understand the difference between investment advisers and stockbrokers, as well as the standards of care pertaining to each. And it’s no wonder, since many titles are thrown around in the investment world — broker, investment adviser, financial advisor, wealth manager, registered representative. How can you make sense of these terms? Let’s focus on two major ones — broker and investment adviser — and examine their roles and responsibilities.

In a 2011 study, the Securities and Exchange Commission found that many investors “expect that both investment advisers and [stockbrokers] are obligated to act in the investors’ best interests” and that there is “confusion by retail investors regarding the roles, titles, and legal obligations of investment advisers and broker-dealers.”

What can be done about this confusion? The first step is to educate yourself. An educated investor is better prepared to protect themselves from financial fraud. So what are the differences between an investment adviser and a broker?

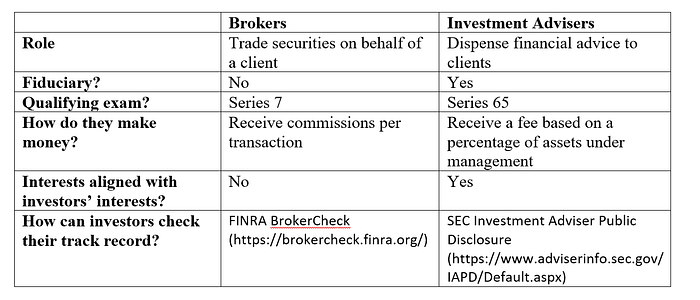

Brokers sell securities to, and make trades on behalf of, investors. To become a broker, one must pass the Series 7 (General Securities Representative Exam), which is a prerequisite to further exams. One must be sponsored by a broker-dealer before registering for the test. Brokers must then register with the Securities and Exchange Commission (SEC) and a self-regulatory authority (most commonly FINRA, the Financial Industry Regulatory Authority).

How do brokers make money? When they sell investment products approved by their member firms, they typically receive a commission, in addition to their base pay. Brokers are not fiduciaries and are not legally bound to act in the best interests of investors; they are bound to only recommend suitable products to investors, but their ultimately loyalty lies with the broker-dealers for whom they work. Some unscrupulous brokers may recommend unsuitable investment products to receive commissions.

FINRA has the primary responsibility for monitoring brokers (and broker-dealers), though the SEC does step in when a risk has been identified. SEC Enforcement could step in if broker-dealers engage in abusive sales practices, fail to disclose material conflicts of interest, make misrepresentations, fail to have a reasonable basis to recommend a certain security, commit fraud, or fail to supervise representatives. Investors should always do their research before working with a potential broker; they should check out FINRA’s free BrokerCheck tool, where one can find out if brokers have been terminated, have had run-ins with regulators, or have had any customer complaints filed against them.

Investment advisers give out financial advice for a fee. Before they’re allowed to do this, however, they must pass the Series 65 exam. Unlike brokers, they don’t need to be sponsored by a firm before registering for a test. Indeed, certified public accountants (CPAs) often take the Series 65 exam to enter the investment advisory space.

How do investment advisers make money? Their compensation is generally fee-based or dependent on a percentage (typically 1%) of assets under management (AUM). This way, the investment adviser’s interests are aligned with those of the client; when the client’s portfolio makes money, the investment adviser makes money. Investment advisers must follow the Investment Advisers Act of 1940, which mandates that they act as fiduciaries, putting the clients’ interest ahead of their own. This high standard of conduct means that most investment advisers can make investment decisions for clients without getting their permission; this is call exercising discretion.

Investment advisers are not the same as financial advisors (which is a generic term, according to FINRA, that often designates brokers/registered representatives). Rather, investment adviser is a legal term designating an individual or company registered with the SEC or a state securities regulator (depending on the amount of assets under management). Per the Dodd-Frank Act of 2011, investment advisers with more than $110 million assets under management (AUM) must register with the SEC (and can do so when they hit $100 million in AUM); Investmnet advisers with assets under $100 million must register with their respective state securities regulator (prior to Dodd-Frank, investment advisers with more than $30 million of AUM had to register with the SEC). If investment advisers fail to disclose material conflicts of interest, make misrepresentations, or commit fraud, SEC Enforcement could step in. To check the track record of a potential investment adviser, investors should check out the Investment Adviser Public Disclosure (IAPD) database maintained by the SEC.

To review the differences between a broker and an investment adviser, let’s look at the following chart:

Of course, not everything is as simple as this chart. Many individuals serve as both investment advisers and brokers. How can you tell? If a broker also serves as an investment adviser, FINRA BrokerCheck will indicate this, as follows:

If you have concerns about your broker or investment adviser, don’t hesitate to contact a securities attorney. Call (877) 238–4175, email info@fkesq.com, or visit www.stopbrokerfraud.com for your free consultation with the securities attorneys of Fitapelli Kurta.